For years, any investor who wished to invest in the markets without having to do a lot of homework, the easy option was to invest in one of the several mutual funds and sit tight. The basic concept here being that the fund manager has a certain expertise and hence will be able to generate good returns on the pool of money so collected.

While ETF’s have a history of their own, it was not until Vanguard hit the scene in 2001 that is started to become more and more noticed as a instrument of choice given the low cost such funds charged.

Over the years, there has been enough of documented evidence to prove that ETF’s may actually be a better tool to invest compared to a Mutual Fund. Both a Mutual Fund and a ETF provide relative returns – in the sense, returns are measured against a set benchmark. While a Mutual Fund manager tries to beat the market to justify his higher expenses, a ETF manager just needs to ensure that the ETF tracks its benchmark as closely as possible.

Unlike a Mutual Fund, a ETF manager cannot and will not buy outside his benchmark to help generate so called “Alpha”. At best, he may vary the weights but even that is not generally entertained given the fact that discretion can cause havoc with the tracking error.

In India, the ETF Industry is still in its infancy with only Nify Bees having some amount of liquidity. Also, there is widespread questioning about whether the Indian Markets are really suited for ETF’s with fund managers claiming that Indian Markets still provide for opportunities for fund managers to deliver Alpha and that ETF’s aren’t the best tool for investing in India.

Its tough to ignore that view since quite a few funds have delivered returns superior to the ETF / Index. But the question is, did they beat while sticking to the benchmark stocks? In majority of the cases, its not.

While Large Cap funds generally benchmark themselves to Nifty or CNX 100 / BSE 100, its not unusual to find in their portfolio names of stocks that are outside the said Indices. In bull markets, its these stocks that provide them the additional reward though in bear markets, they do have the ability (as shown in the fall of 2008) to drag the fund performance even below its Benchmark returns.

The question that one does come to finally is that if a Investor is able to split his investments between Large Cap ETF’s (Nifty Bees for instance) and ETF’s tracking Indices such as CNX 100 / CNX 500, would he be able to generate better returns.

A list of ETF’s (Equity) listed on the NSE can be found here (Link)

While both Nifty and CNX 100 are represented, its disappointing to see no ETF’s tracking the broader CNX 500 Index. Either way, unless there is more interest in ETF’s its doubtful to see fresh ETF’s being launched.

To decipher whether by dividing our capital, we can generate returns similar to the best mutual funds, I used Nifty Bees for Nifty and the respective Indices, CNX 100 and CNX 500. Since NSE does not provide total return Indices for Indices other than CNX Nifty, I used the general Index.

The key difference is that in all the above tickers I have used, I have not accounted for dividends that get paid. While small, these do have a impact on the overall returns if the same is invested back.

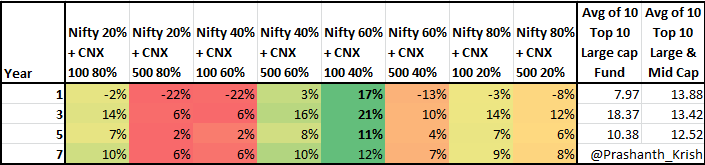

To answer the question as to how much one should invest in Nifty and how much in a CNX 100 / CNX 500 ETF, I drew the following matrix

The returns generated above are CAGR returns (without accounting for Dividends). In case of Mutual Funds, all the selected were Growth Schemes

Top 10 Mutual Funds are selected based on Category and look back period. So, 18.37% represents the average return of the top funds over the last 3 years. Now, a few may be in the other brackets and a few others may not be. Idea was to select and compare with the best possible (which is known only in hindsight) options.

Even in the above matrix, there are issues when it comes to comparing against ETF’s. For instance, the the top performing fund on the 1 year look back was ICICI Prudential Advisor Series -Very Aggressive Plan (G). Now, the plan is more of a Allocation Model with 80% of its funds being invested in Debt and only 20% in Equity. Its no wonder that even as the broader market showcased negative returns, this generated strong Alpha.

As the above table clearly lays out, investing 60% in CNX Nifty tracking ETF and 40% in CNX 100 tracking Index provides the best return which beats the return of almost all Mutual Funds. And best of all, you do not need a Advisor to guide you since all it requires is a call to your broker and buy the concerned ETF’s in the proportion that one is acceptable with.

And when it comes to the question of how much to invest, do take a look at our Allocation Matrix (Link). All in all, investing is simple, all it requires is a bit of discipline and hard-work of buying and you can be your own fund manager.

The biggest advantage of a ETF over Mutual funds is the fact that you can exit whenever you want without having to worry about paying load (which can be pretty huge) due to the short amount of time spent with the fund. This allows for better allocation as you can move in and move out without the need to wait for the minimum time to elapse.